All Activity

- Today

-

How to mint Nft in bc.game?

How to mint Nft in bc.game? -

trendslookup joined the community

-

A real estate lead generation agency helps property businesses attract qualified buyers and sellers through targeted marketing strategies. They use SEO, paid ads, social media, and email campaigns to capture and nurture leads. By analyzing audience behavior and market trends, these agencies deliver high-quality leads that boost sales and ROI. Partnering with a professional lead generation agency ensures consistent growth, stronger brand visibility, and better conversion rates in the competitive real estate market.

- Yesterday

-

Привет, вот жду когда вернут.

-

Привет, форум.

-

Wlualjeakwb joined the community

Wlualjeakwb joined the community -

Axelito200 joined the community

Axelito200 joined the community -

How can i gef the $4

-

Lwdoygmyzwcc joined the community

Lwdoygmyzwcc joined the community -

Pdtaofgrkvcc joined the community

Pdtaofgrkvcc joined the community - Last week

-

Yhpajhrdrycc joined the community

Yhpajhrdrycc joined the community -

Ziidhhyfdycc joined the community

Ziidhhyfdycc joined the community -

Icloudss joined the community

Icloudss joined the community -

-

Vqphbhbicxcc joined the community

Vqphbhbicxcc joined the community -

Visit Our Site Now - https://hiringgo.com/services/recruitment-agency-in-delhi Finding the right talent is crucial for any organization’s growth, and a reliable recruitment agency in Delhi can make this process seamless. Our agency specializes in connecting businesses with skilled professionals across various industries, ensuring that every hire aligns with your organizational goals and culture. We understand that Delhi, being a hub for commerce, IT, finance, and startups, demands a recruitment partner who can deliver quality candidates efficiently and effectively. Our team of experienced recruiters leverages advanced sourcing techniques, including talent mapping, headhunting, and database searches, to identify the best candidates in the market. We cater to diverse sectors, including IT, finance, healthcare, manufacturing, and more, providing tailored recruitment solutions that meet both permanent and contractual staffing needs. By understanding the unique requirements of each client, we ensure a perfect match that drives productivity and reduces employee turnover. At our recruitment agency in Delhi, we prioritize candidate experience just as much as client satisfaction. Every applicant is carefully screened, interviewed, and assessed to ensure they possess the right skills, experience, and attitude to thrive in your organization. Our commitment to excellence extends to providing guidance on market trends, salary benchmarks, and industry insights, empowering companies to make informed hiring decisions.

-

HiringGo joined the community

HiringGo joined the community -

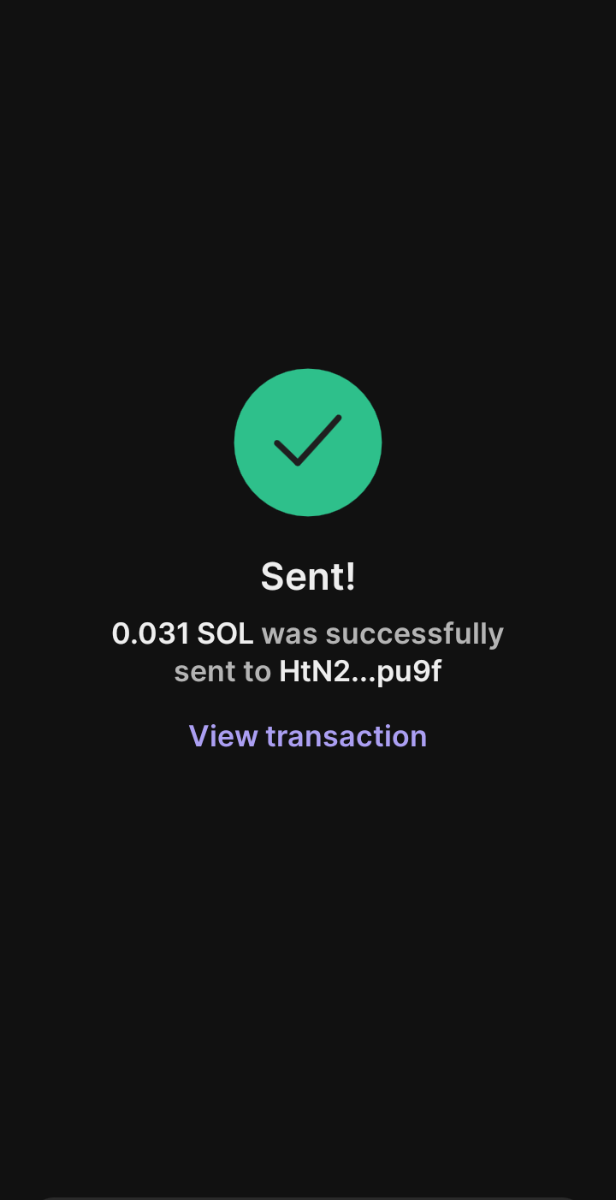

Hi Guys, My solana deposit is still not credited to my account. Please help. There is no way to use the chat as well. No email support too.

-

hii

-

NBA | Indiana Pacers vs Milwaukee Bucks - Jan 28 | 00:00 UTC

Zinavo replied to Mat's topic in Sports Discussion

The Indiana Pacers face off against the Milwaukee Bucks on January 28 at 00:00 UTC in a thrilling NBA matchup. Expect fast-paced action as both teams battle for dominance in the Eastern Conference standings. -

Greetings to all!I had to register to leave a review of my experience on this site.9378836 - This case has been open for a week. The issue is that my deposit became problematic due to a usdt memo on the ton network. The memo has now been removed, but the problem remains.I've been writing all week hoping for updates, but support is completely helpless. I only get a generic message about the importance of patience, how they appreciate and understand me, and are generally on my side. But they can't give me any timeframes, because my key is "a priority," and they've been working with the entire team to resolve it, but they can't seem to find a solution. I've also been using the check-in bonus on Telegram all week. Today is Sunday, and I was supposed to receive my reward (I thought I'd at least be able to play that way), but I haven't received it, and honestly, I'm not even surprised.And the apogee of it all is today's communication with support. I approached them with a reasonable question: I want to play, how do I do it? I can't play with my own money or with bonus money, because neither works. Please give me a solution! And you know what I get in response? The agents leave the chat; they simply stop responding and leave the chat!)))I've never encountered such a service! They don't offer any kind of personal bonus in their chat for this kind of situation, or any kind of compensation while I'm forced to wait. They claim their entire team can't resolve the issue, and they can't provide any recommendations or deadlines.Overall, it was humiliating trying to play in bc.game. Peace and blessings to all.

-

Hellos from the noobs

-

I NEVER COME ACCROSS ANY SHITCODES OR PROMO CODES.... EVER

HObbs51 replied to WinBigToday2020's topic in User Events & Promos

Help -

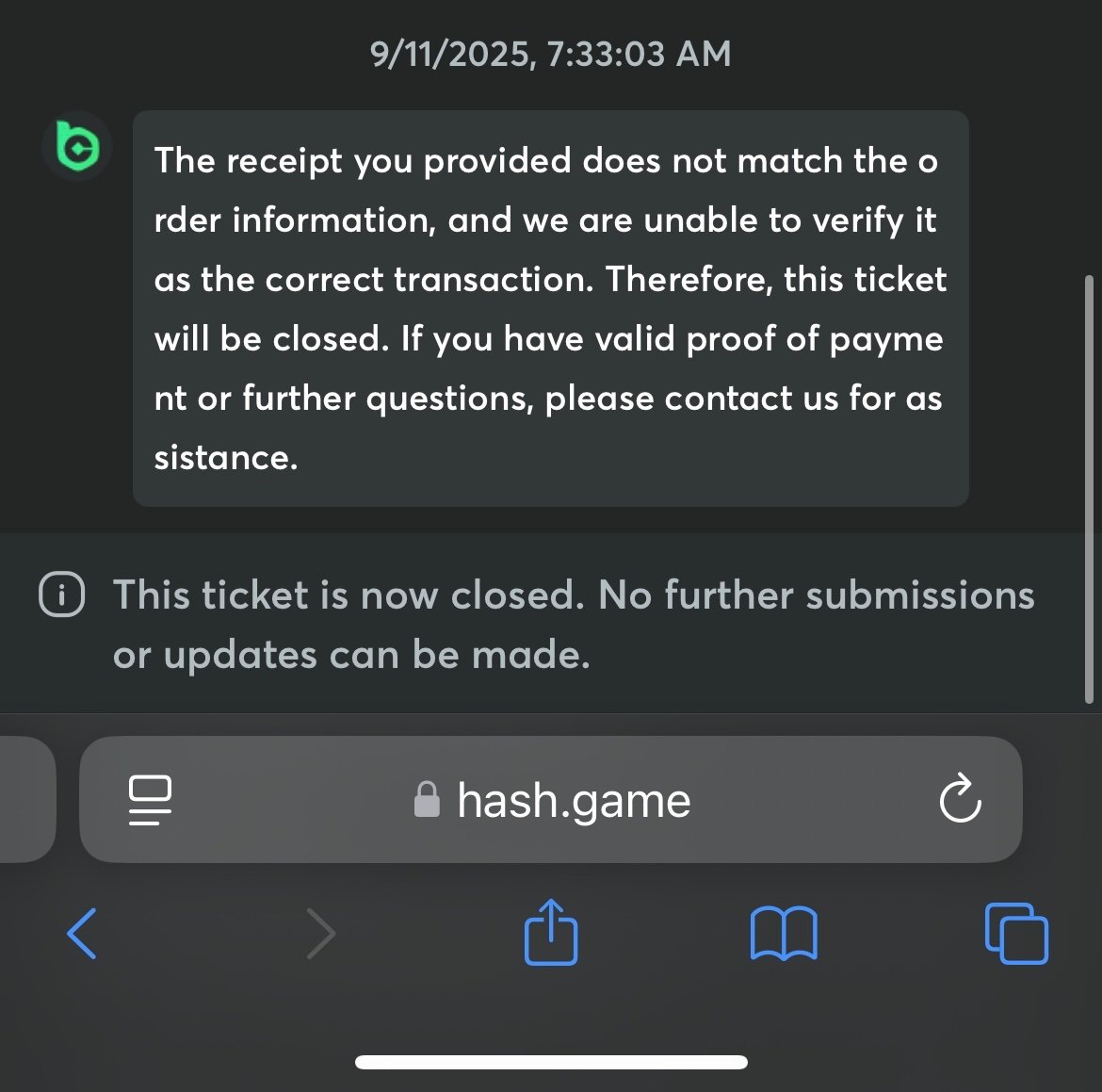

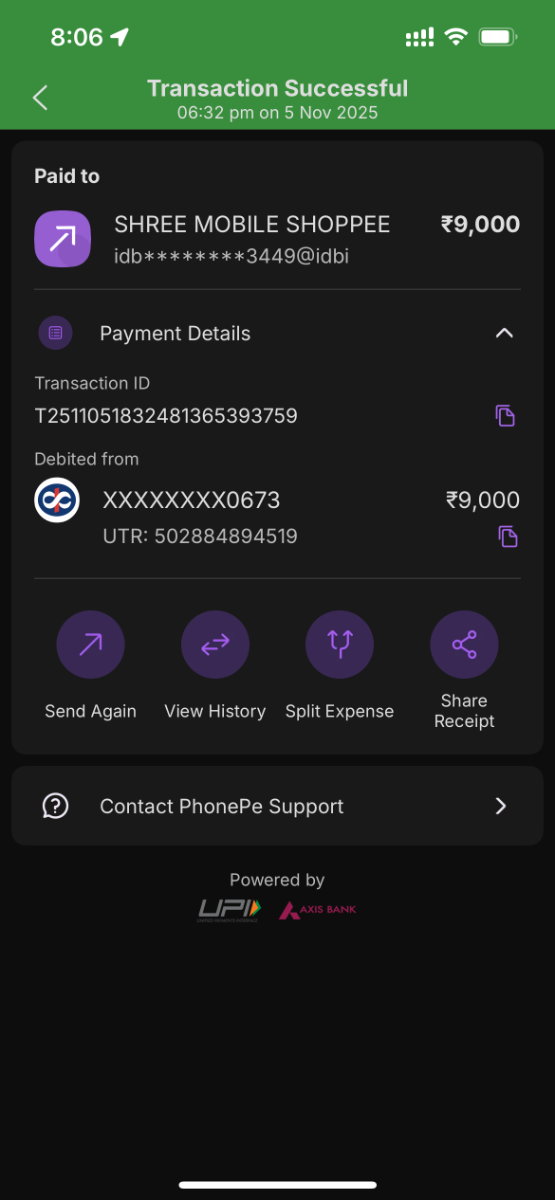

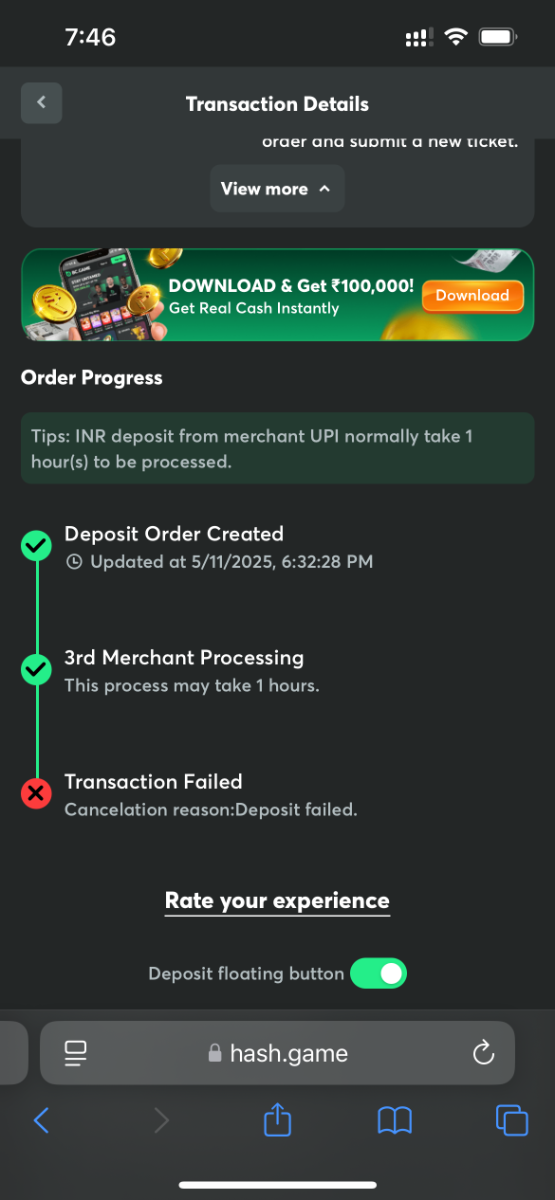

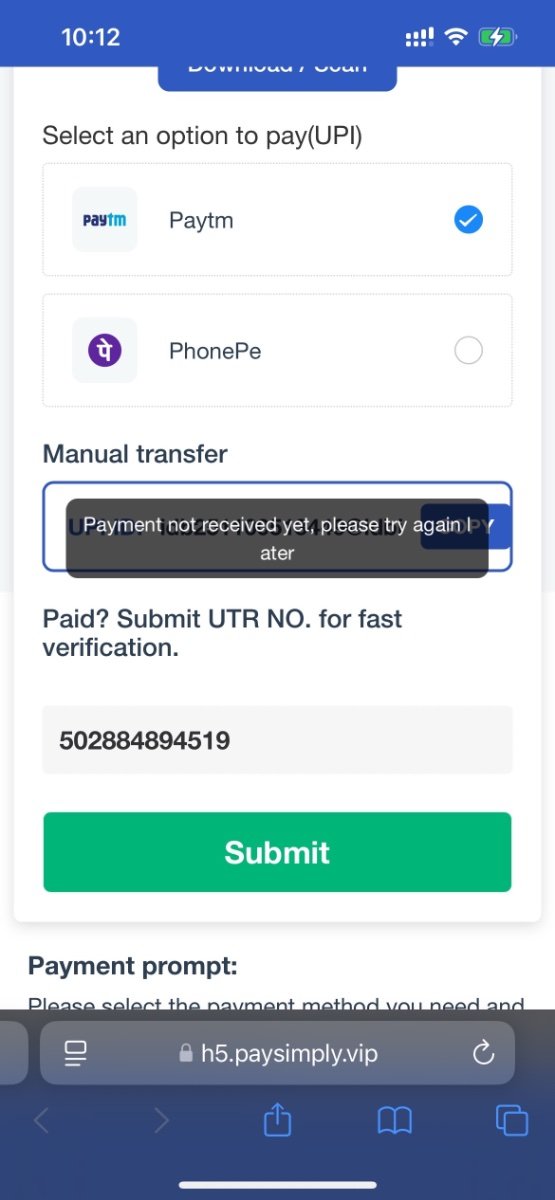

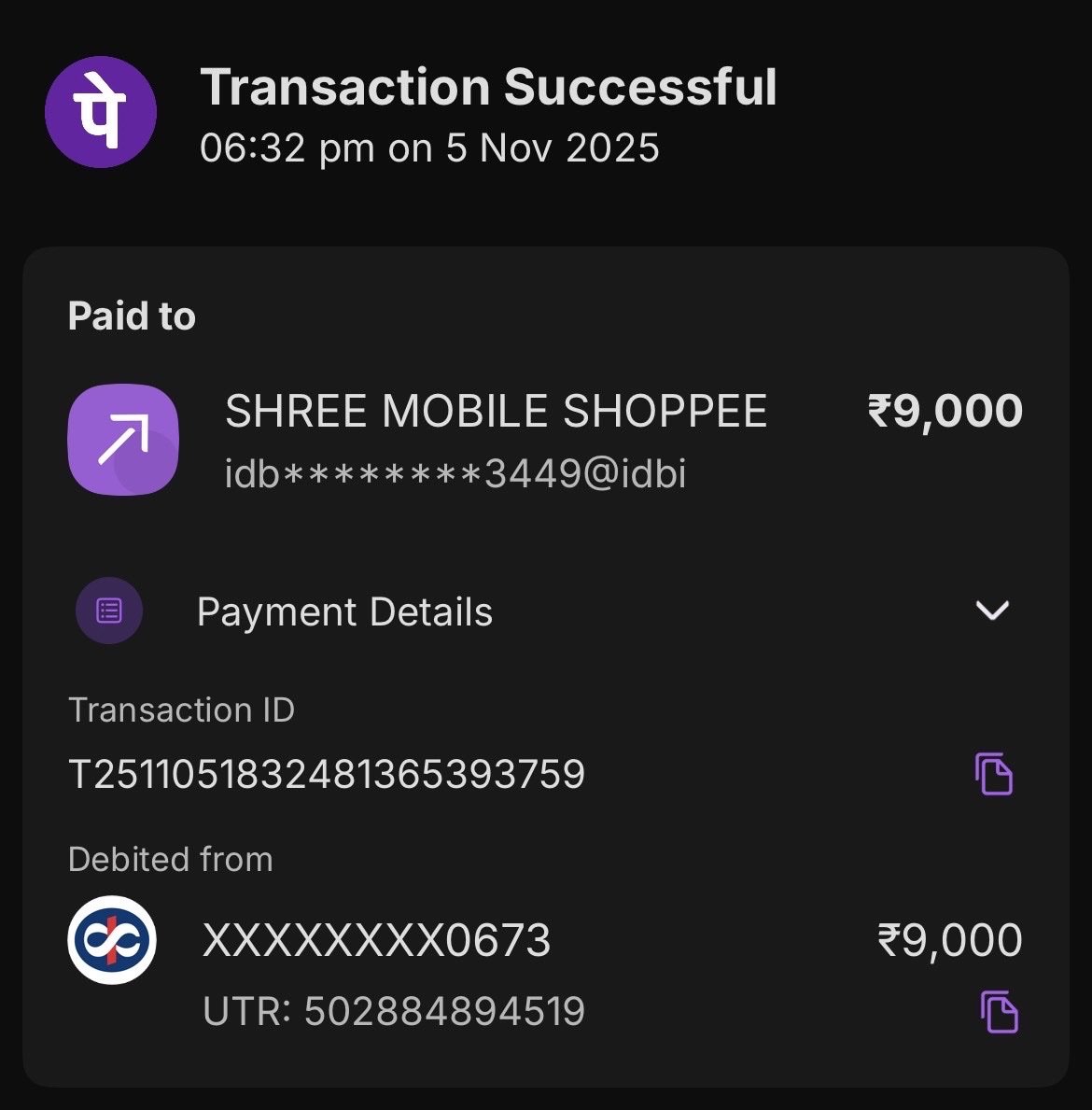

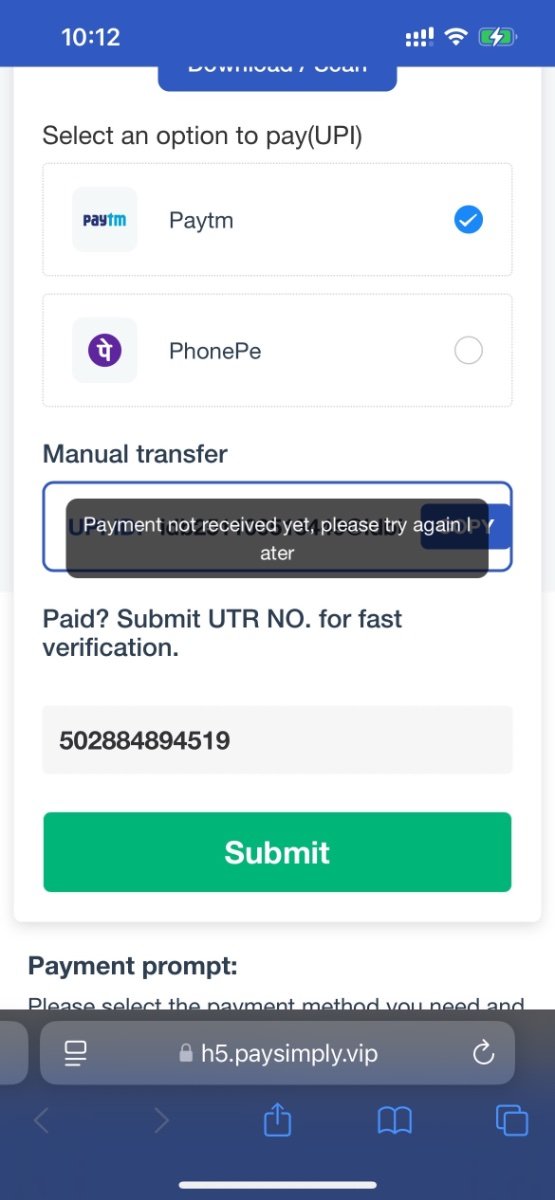

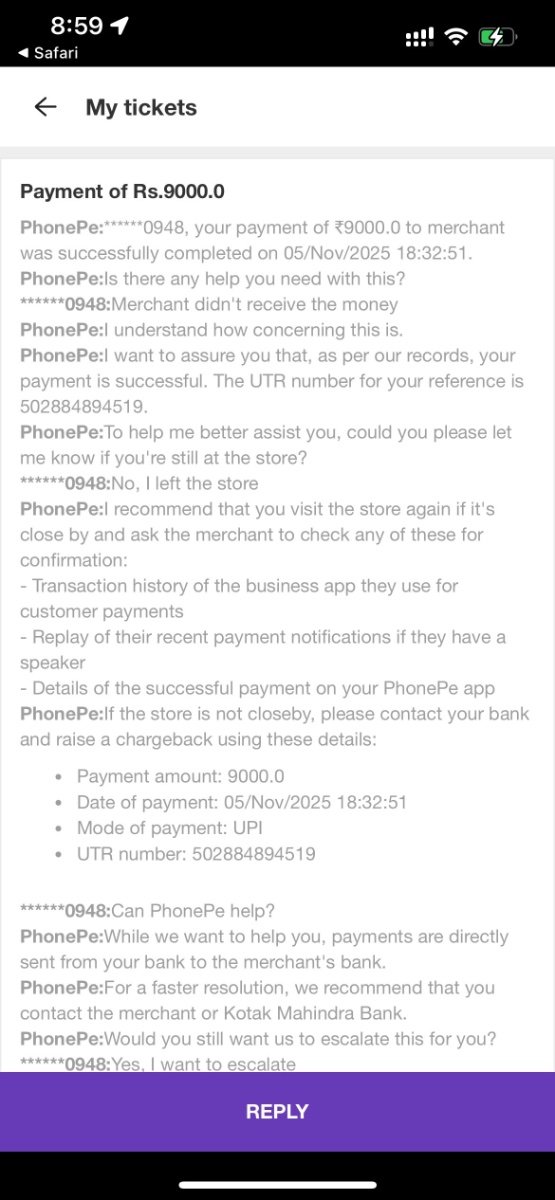

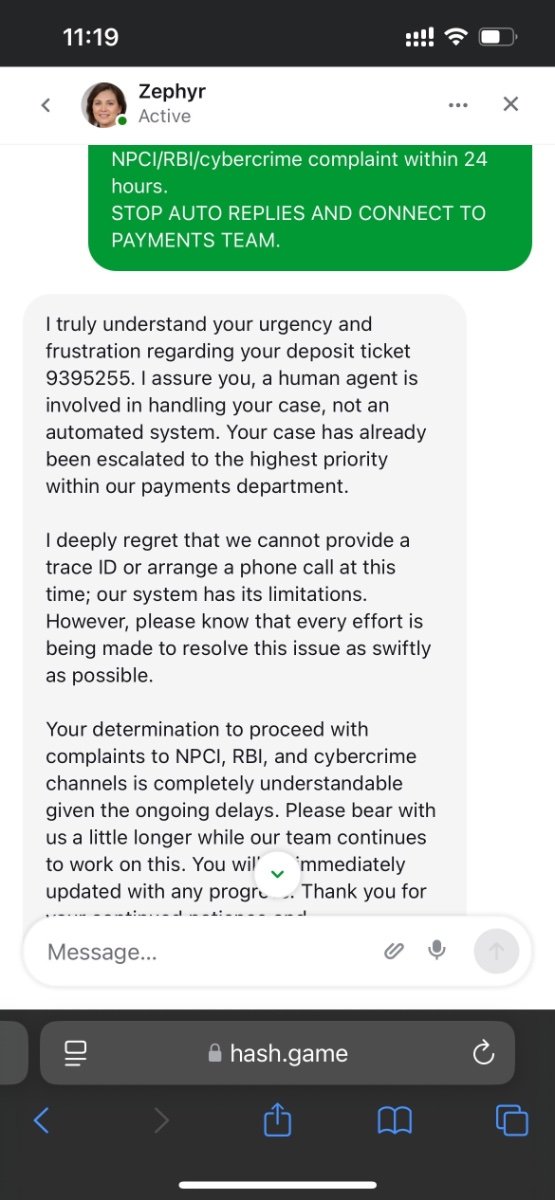

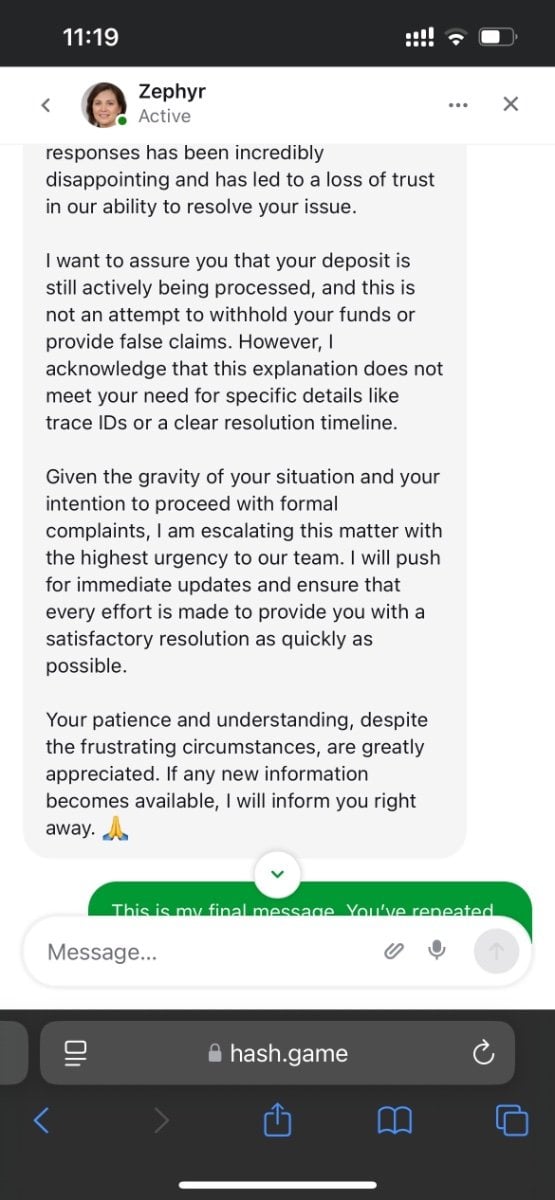

you closed my ticket #9395255 without solving anything. I never asked to close it. ₹9,000 deposit from 5 Nov (UTR 502884894519 / UID 99007906) still missing. Stop hiding behind bots and fix this. #BCGame #UPI #Scam

-

This is not the first time I’m facing this nonsense. On 8 September, I made another deposit of ₹1,000 that you never resolved — not even after two months of waiting and following up. That was frustrating enough, but now ₹9,000 missing? This is ridiculous and completely unacceptable. If this is how you handle user funds, then you’re putting your entire credibility at risk. I’m not going to sit quietly this time — either credit the ₹9,000 to my account immediately or refund it back to my payment source without further excuses. I have attached the PhonePe transaction proof showing the successful payment. I expect a proper resolution, not another generic response. Handle this seriously — this is the second time, and I will not let this go ignored. Bc game id 99007906

This is not the first time I’m facing this nonsense. On 8 September, I made another deposit of ₹1,000 that you never resolved — not even after two months of waiting and following up. That was frustrating enough, but now ₹9,000 missing? This is ridiculous and completely unacceptable. If this is how you handle user funds, then you’re putting your entire credibility at risk. I’m not going to sit quietly this time — either credit the ₹9,000 to my account immediately or refund it back to my payment source without further excuses. I have attached the PhonePe transaction proof showing the successful payment. I expect a proper resolution, not another generic response. Handle this seriously — this is the second time, and I will not let this go ignored. Bc game id 99007906

-

-

?

-

Bonus

-

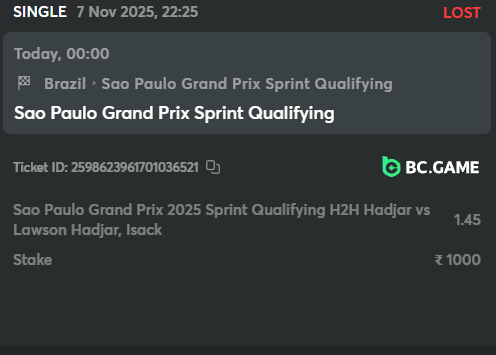

Hi guys, I have placed the bet on Hadjar to win F1 sprint Qualifying H2H Hadjar vs lawson. Hadjar finished 9th and lawson on 17th but my bet has lost. what should I do I cannot connect the customer support also.

-

I can make any script you want

-

I can do that. I can make any script you need

- Earlier

-

-

I’ve always believed that taking care of your car is a lot like staying fit for sports — performance depends on consistent maintenance, premium care, and attention to detail. Recently, I came across a few specialized automotive brands in Dubai that treat cars with the same passion athletes put into their training: Carzilla Motors – for anyone looking to buy or sell luxury cars in Dubai. They’ve got amazing collections of pre-owned BMW, Mercedes, and Range Rover models. Carzilla Car Care – this one focuses on ceramic coating, paint protection film (PPF), and car detailing for high-end cars. The level of precision reminds me of Formula 1 pit crews. Carzilla Auto Service – great for Car repairs and Auto servicing. It’s like having a fitness coach for your car’s engine. Cars, like athletes, perform best when they’re trained, maintained, and protected. If you’re in Dubai and love your ride as much as your sport, these guys are worth checking out.

I’ve always believed that taking care of your car is a lot like staying fit for sports — performance depends on consistent maintenance, premium care, and attention to detail. Recently, I came across a few specialized automotive brands in Dubai that treat cars with the same passion athletes put into their training: Carzilla Motors – for anyone looking to buy or sell luxury cars in Dubai. They’ve got amazing collections of pre-owned BMW, Mercedes, and Range Rover models. Carzilla Car Care – this one focuses on ceramic coating, paint protection film (PPF), and car detailing for high-end cars. The level of precision reminds me of Formula 1 pit crews. Carzilla Auto Service – great for Car repairs and Auto servicing. It’s like having a fitness coach for your car’s engine. Cars, like athletes, perform best when they’re trained, maintained, and protected. If you’re in Dubai and love your ride as much as your sport, these guys are worth checking out.

.thumb.jpg.388889424acc85bbeb79afdaaa1e18d3.jpg)